While private equity is no stranger to dermatology having been invested in the specialty for ~10 years, the opportunity for dermatology practices to partner with private equity has never been more abundant. Although 2021 has seen over 25 practice acquisitions year-to-date, the broader dermatology sector remains highly fragmented with only 12% of the market consolidated today with dermatology private equity backed groups. The remaining level of fragmentation exists alongside a multitude of strategic alternatives. In the private equity realm, success stories such as Advanced Dermatology & Cosmetic Surgery, Forefront Dermatology, and Water’s Edge/Riverchase Dermatology (recently merged) have validated that specific model with successful “second-bite” exits, driving interest from practices across the country. Currently, there are over 30 private equity-backed platforms throughout 18 states. That number is expected to keep growing as consolidation within the space continues to mature. All that said, it is important to note that not all partnerships are successful in this space. Understanding the value in company culture and aligned strategic vision in each potential partner is equally important than just the economic value they present.

The Private Equity Strategy

While private equity firms vary significantly regarding fund size, strategy and resources, all initial investments into the space are made with the intention of helping their physician partners achieve economies of scale. This is done through both organic growth & geographic expansion, inclusive of add-on acquisitions, de novo expansion, and the enhancement of ancillary services. To ensure this is done in the most efficient and effective manner, dermatology private equity backed groups employ highly experienced operators at both the board and practice level. Through strategically deployed capital, experienced operators, and physicians that can focus solely on delivering exceptional clinical outcomes, the creation of scale can be expedited. The result is partners across the footprint benefitting, both clinically and financially, while simultaneously driving returns for their private equity backer. Dermatology private equity backers are determined to achieve their target return on investment (ROI) and understanding how they plan to achieve their goal is essential to a successful partnership. It is groups that sacrifice patient outcomes for short term economic gain, or do not have an established growth vision tend to fail. Understanding the broader competitive landscape and strategic vision of financial and strategic partners is paramount before entering a transaction.

Once an inflection point is achieved, the private equity backed dermatology group will look to sell the platform to a new financial partner that may or may not already have an existing dermatology business. This second sale will generate a “second bite of the apple” for physician shareholders which, assuming a successful partnership, leads to another successful economic outcome or “Third bite of the apple”. Examples of such are Forefront Dermatology and Advanced Dermatology and Cosmetic Surgery who have both experienced major liquidity events with their “second bites” and are well on track to their third sale.

While the dermatology private equity strategy has multiple successful examples in the space (as aforementioned), there are groups that have struggled comparatively. Groups like DermOne lacked success for various reasons, but even in these scenarios’ opportunity remains. As the private equity dermatology consolidation wave continues, the largest, most successful groups in the space have, and will continue to, acquire those that tried and failed to do the same. The result is the initial hoped-for outcome the physician shareholders were looking for at the outset, albeit at a slower pace.

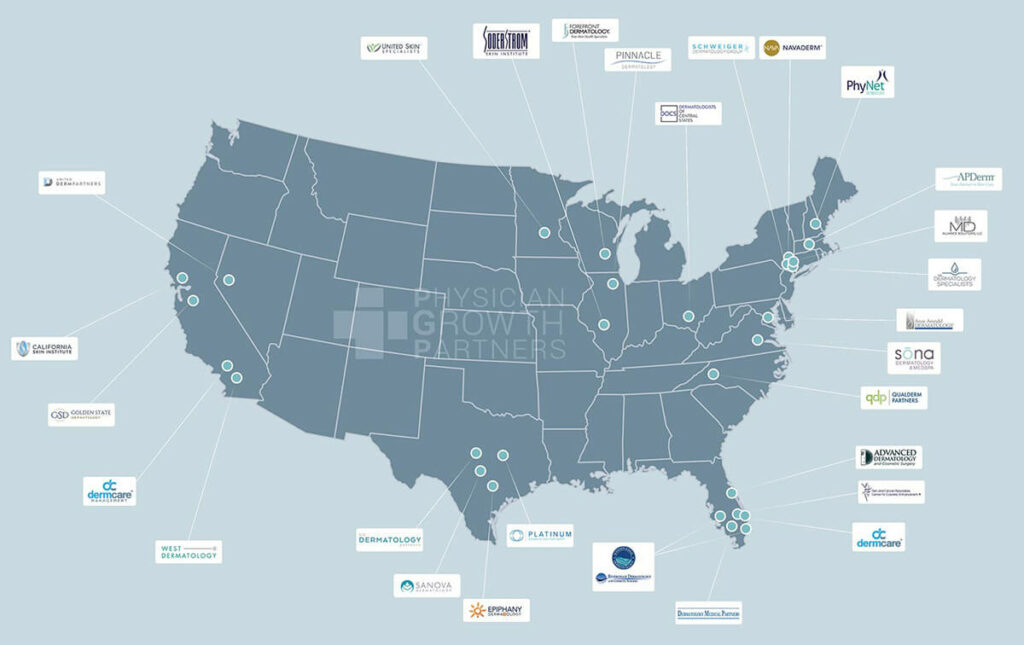

Consolidation Landscape to Date

Private Equity Initial Investments*

*Shows markets where the platform has a presence in, does not include all locations

Why Now

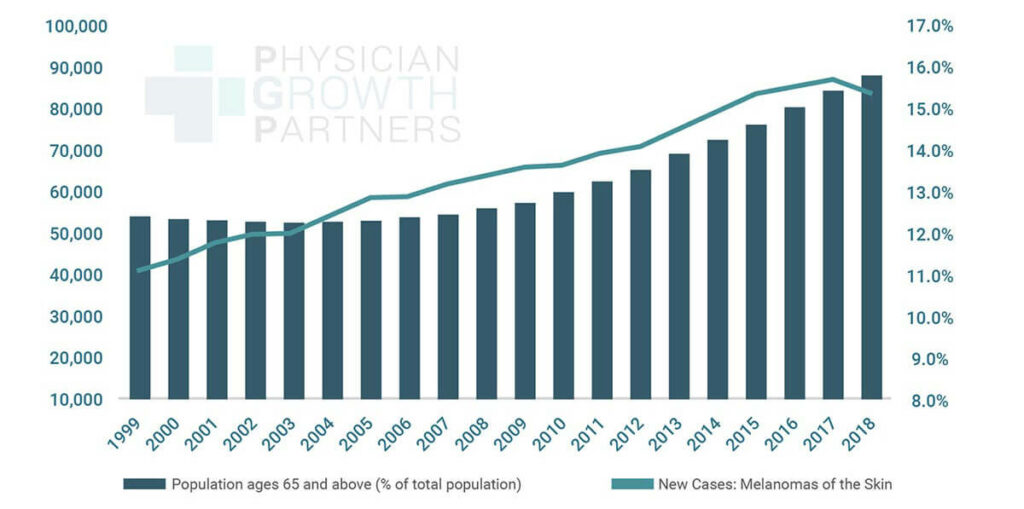

The dermatology industry has seen significant growth due to an again population, increased awareness of skin disease, and increased demand for elective cosmetic procedures. For example, it is estimated that 1 in 5 Americans will develop skin cancer by the age of 70, and by 2029 20% of the US population will be over the age of 65. This shift in age demographics coupled with widespread market fragmentation is a major factor contributing to recent and continued growth.

New Melanoma Cases VS 65+ Population

Source: The World Bank DataBank | Centers for Disease Control and Prevention United States Cancer Statistics

Despite private equity’s longstanding presence in dermatology, particularly when compared to other specialties private equity has invested in, it is estimated that ~75% of dermatology practices have less than five physicians. While demand for dermatology services continues to increase at the macro level, practices are more frequently turning to dermatology private equity backed groups for the comprehensive infrastructure, physician network and strategic capabilities they can provide. With the dermatology landscape evolving it is becoming more challenging for smaller practices to compete. Groups are heavily motivated to transact in an effort to control their own destiny while they still maintain leverage in their respective markets. Further fueling that interest is the fact that dermatology groups of all sizes continue to receive premium valuation consideration as established private equity backed dermatology platforms across the country look to expand their success in existing and new markets. Competition and success amongst private equity backed dermatology platforms is driving very seller-friendly deal structures along with attractive economic consideration, making the private equity option increasingly appealing.

How Are Independent

Physicians Impacted?

Private Equity partnership has been attractive option for independent sub-specialty physicians across specialties for the last decade. Interest has amplified as the private equity model has evolved and adapted to mistakes made in the past while building upon previously established best practices. The capital support and strong leadership offered by private equity groups alleviate many of the administrative and financial responsibilities burdening independent physician practices, allowing dermatologists to focus exclusively on providing high quality clinical care in an increasingly complex environment. While the realities of the private practice of medicine are evolving rapidly, so is the macroeconomic environment. Low interest rates and high levels of uninvested capital have created an environment ripe for acquisition activity. As these conditions continue to evolve, private equity activity will only continue to accelerate. While the right private equity model is focused on insulating independent physicians from external forces, improving the quality of medicine, and creating economic opportunity, the establishment and growth of private equity backed platforms adds another layer of pressure for those that choose to remain entirely independent. Again, these partnerships are not always successful. No two transactions are the same and not all partnerships result in success. Independent physicians must rely on all their resources to ensure appropriate due diligence is performed, a strategic vision & plan is approved, and deal terms are advantageous for themselves.

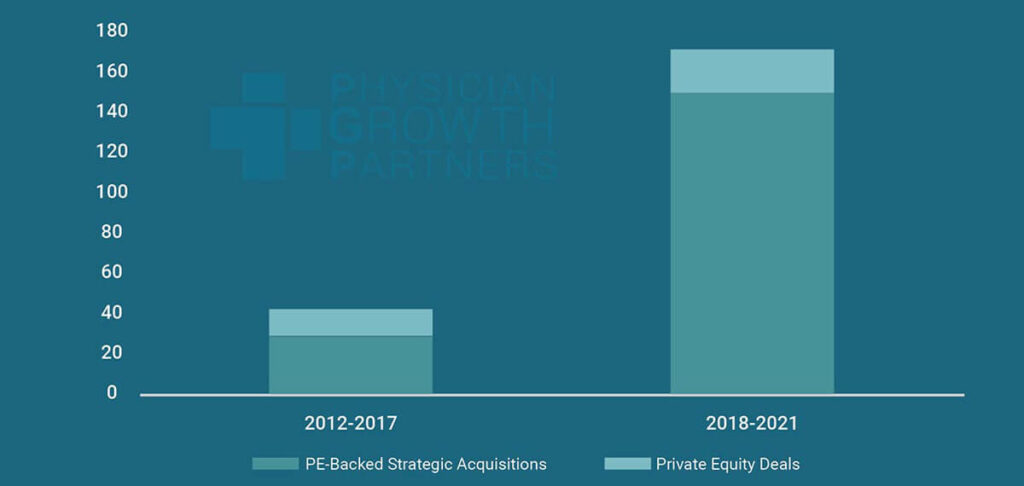

Private Equity In Dermatology

Source: PGP Proprietary Deal Tracker

What Happens After The Transaction?

One of the biggest questions practice owners have is what happens after the transaction is consummated? In reality, physicians will largely continue to operate “business as usual”. The private equity partner will look to implement certain growth initiatives, but these initiatives will all be items that were discussed at great length in advance of consummating the transaction. On the clinical front, physicians will practice medicine the way they always have. Clinical autonomy is almost always maintained. The only changes that occur should be additive. As for infrastructure capabilities, groups that lack back-office sophistication will typically integrate into the “platform” practices EMR, Accounting and PM systems.

Outside of day-to-day operations and clinical delivery, the most notable change is the holding of rollover equity in the new partnership by selling physicians. Due to the fact a substantial liquidity event is experienced, shareholders are required to utilize a percentage of their proceeds in the form of equity in the new enterprise. This is desired by the Private Equity firms as they want to maintain alignment with the physicians that they have invested in, creating a shared goal of a “second bite of the apple” when the platform ultimately experiences a subsequent sale 3–7 years down the road. While achieving a great economic outcome in your initial sale is great, PGP always stresses partnership over value as a successful partnership should lead to an even greater economic event down the road as private equity firms typically underwrite a 3-5x return on equity.

As mentioned above, for groups that decide to go down the Private Equity path, nothing is more important than clinical and strategic fit. The successful thesis that is playing out in today’s environment requires shareholders of all types (physicians, investors, operators) to do what they’re best at – doctors need to practice medicine, operators need to oversee the business, and investors need to make sure capital that has been put to work is generating value while keeping additional capital available for strategic deployment. The result when done right is groups that deliver the highest level of clinical care – which should be the top priority for everyone involved – expanding that level of care, and driving significant, sustainable value

Working with Physician Growth Partners

Physician Growth Partners is a firm that recognizes and prioritizes the importance of clinically focused outcomes, first and foremost. The groups that allow us to advise them will attest to the fact that we always emphasize partnership over economics. When the highest level of care is delivered, financial success will always follow.