Within the landscape of healthcare investing, Pain Management specialty practices have seen amplified levels of interest from private equity investors since 2020. Despite this interest, compared to other specialties that are further along in the consolidation life cycle, Pain Management care has yet to experience large scale M&A efforts. The total number of transactions in 2021 was six, following only two in 2020 and only five in 2019. Comparatively, specialties like orthopedics and gastroenterology have each seen 50+ and 60+ transactions since the start of 2021, respectively.1

One driver of consolidation across all physician practices is the cost synergies that naturally arise with operational scale. The combination of these synergies and the parallels that can be drawn between Pain Management and other sub-specialties has begun to attract private equity investment. With a sub-specialty as fragmented as Pain Management, private equity groups are looking to leverage size and scale by creating provider density, bringing ancillary services in house, centralizing infrastructure and operations, and streamlining payor negotiations.

Private Equity Backed Pain Management Landscape

Why Now

Pain Management has quickly become one of the most attractive sub-specialties for private equity investment as accessibility and quality has become increasingly prevalent. First, aging demographics in the United States continues to drive an increase in demand for Pain Management services. As the U.S. population continues to age, joint replacements, spinal complications and related cases have continued to rise nationally. For example, the United States Joint Replacement Market size was estimated at $3.62 billion in 2021, expected to reach $3.97 billion in 2022 and is projected to grow to reach $5.19 billion by 20272. These procedures are all related to the need for Pain Management services.

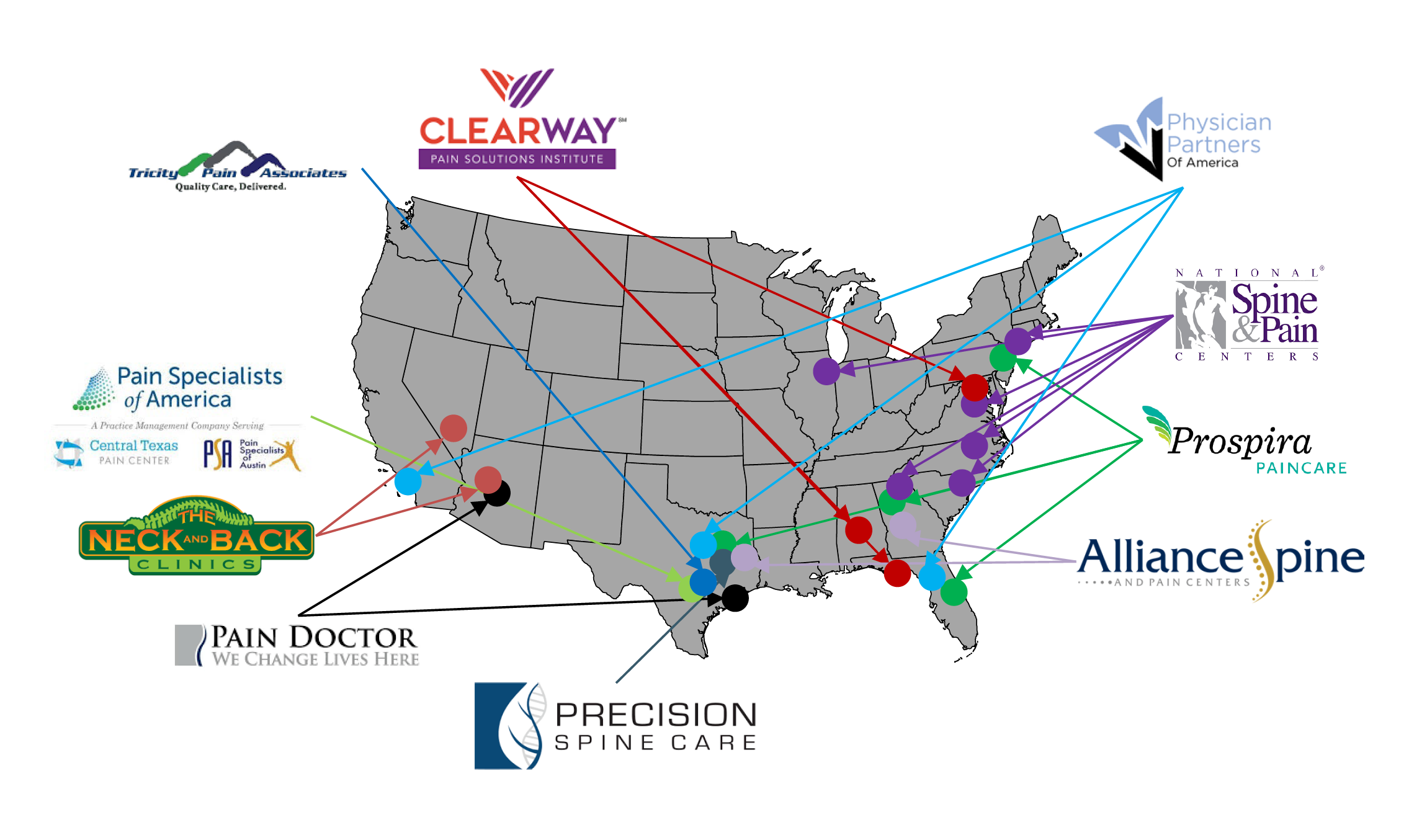

Additionally, Pain Management care remains one of the most fragmented sub-specialties in U.S. healthcare. It is estimated that nearly 70% of Pain Management practices have fewer than 10 providers3. Notably, there is a lack of established, scaled Pain Management platforms within major U.S. metro markets and their surroundings. Currently, 15 platform organizations exist, serving major markets in the Southwest, Southeast, Mid-Atlantic and Northeast4. These facts, coinciding with the ongoing push towards outpatient procedures that offer quality of care, affordability, and increased accessibility has created an environment ripe for independent practices and private equity to take advantage. That said, only recently has the attention from private equity in the Pain Management space been widely reciprocated by doctors.

With a plethora of service offerings, there are many opportunities for sustained growth among private equity-backed Pain Management platforms. Primary pain care, medication management, drug screening, DME, regenerative medicine all offer a variety of ways that platforms can create “one-stop-shop” opportunities for private practices seeking growth.

The depth of Pain Management service offerings also creates a value proposition that private equity can offer Pain Management specialists. The introduction, expansion, and enhancement of services private equity can support allows for greatly accelerated growth, and in turn, a benefit physician shareholders can reap on an ongoing basis. Looking at the broader picture and the recent increase in interest from independent Pain Management specialists, activity is expected to rapidly accelerate in the next 5 to 7 years. This creates an attractive but narrowing window of opportunity for independent practices to become first movers and leaders within their geographic landscape.

The Private Equity Strategy

The overall drivers of private equity investment are similar between sub-specialties, but the underlying strategies vary from group to group. Groups are looking to enter markets with a scaled, clinically excellent provider, then build around them in that region. Whether it be through de novo/acquisitive growth or service line expansion, PE backers will use their resources to build density around a founding partner in each region. Each platform may have different preferences as to how they achieve economies of scale, but that will always be their goal.

When it comes to building an effective growth strategy, private equity platforms are seeking out physicians, experienced operators and industry veterans that are well-versed in sourcing, evaluating, and eventually consummating partnership opportunities. Through strategic planning, deploying ample capital and aligning providers, optimal outcomes can be achieved from both a clinical and financial standpoint. Private equity backers seek to achieve target ROI over an extended growth cycle that is typically 3 to 7 years, so operational shortcuts are not an option for investors. Maintaining quality care is at the forefront of each platform’s strategy, but it is very important to understand the underlying vision of each potential partner before entering a transaction.

Once an inflection point is achieved, a private equity-backed Pain Management group will look to sell the platform to a new financial partner that may or may not already have an existing Pain Management business. This sale will generate a “second bite of the apple” for physician shareholders that, assuming a sound partnership, leads to another successful economic outcome or “third bite of the apple” down the road. These sales may occur in a variety of ways, including selling to another existing platform, a larger healthcare-focused fund, or by potentially going public. This sale is frequently referred to as a “second bite,” triggering a liquidity event for physicians to achieve a successful economic outcome or roll their equity over to the new platform sponsor. Pain Management has yet to experience large scale “second bites,” proving that it is a specialty that has a substantial runway for growth in the future.

How are Independent Physicians Affected?

Whether physicians prefer to be hands-off or take part in strategic planning, there are platforms that offer a full range of options. Practices at the local level are most often encouraged to be as involved as possible to plan for target market entries and future service offerings. One of the most pressing questions that comes from physicians interested in a partnership opportunity is how the transaction will affect their day-to-day operations and overall quality of life. Private equity sponsors have become an attractive route for providers by relieving some of the headaches associated with business development, administrative duties, and clinical care. Most platforms understand that partnerships are not “one size fits all,” and work to achieve the goals of providers in all aspects of the business.

Private Equity partnership has been an attractive option for independent sub-specialty physicians across specialties for the last decade. Interest has amplified as the private equity model has evolved and adapted to mistakes made in the past while building upon previously established best practices. The capital support and strong leadership offered by private equity groups alleviate many of the administrative and financial responsibilities burdening independent physician practices, allowing Pain Management specialists to focus exclusively on providing high quality clinical care in an increasingly complex environment.

Driving Practice Value

With extensive experience negotiating opposite the PE buyer universe, Physician Growth Partners delivers results to all clients that exceed market expectations and go beyond what could have been achieved on a standalone basis. An essential aspect of how PGP drives value lies in utilizing a competitive process. With a carefully curated set of prospective partners involved, we help clients understand how each option can help achieve the practice’s goals, both in the short and long term. Utilizing a healthcare transaction advisor like PGP gives physicians the ability to focus on clinical operations while an experienced, independent team crafts the optimal partnership strategy to achieve their goals.

While the starting point of establishing transaction value begins with financials, there are a multitude of factors both qualitative and quantitative in nature that influence purchase price. Established operational infrastructure, a market reputation, and attractive growth prospects can all raise valuations. Physician Growth Partners utilizes our team’s financial acumen and our market knowledge to accurately measure what buyers will give “credit” for. This ensures our client will achieve an optimal value.

What Happens After the Transaction?

One of the biggest questions practice owners have is, “What happens after the transaction is consummated?” The answer is, physicians will largely continue to operate “business as usual.” Private equity partners will look to implement certain growth initiatives, but these initiatives will all be items that were discussed at great length in advance of consummating the transaction. On the clinical front, physicians will practice medicine the way they always have. Clinical autonomy is almost always maintained. The only changes that occur should be additive. As for infrastructure capabilities, groups that lack back-office sophistication will typically integrate into the “platform” practice’s EMR, Accounting and PM systems.

Transacting with a private equity sponsor can seem like a daunting transition—in reality, physicians will largely continue to operate their practice in a “business as usual” manner. Sponsors will work to incorporate strategic growth plans, but in Pain Management, where much of the decision making is made at the local level, a great deal of autonomy remains. Operationally, platforms offer guidance to help practices enhance their workflow. All changes that occur should not strip away what has been built up since the inception of the practice. Infrastructure will be bolstered, and back-office operations will likely be integrated into the platform to improve efficiency. On the clinical front, physicians will practice medicine the way they always have. Clinical autonomy is among the most important factors for physicians interested in a partnership. PGP emphasizes this and platforms understand its importance.

Private Equity Value Creation

Gaining Payer Leverage

Capturing In-House Ancillary Services

Centralizing Infrastructure and Operations

Resulting In

Sustaining Organic Growth

The last element of the transaction that is important to note is the equity that is rolled over into the new partnership by practice shareholders. Platforms expect that a percentage of the purchase price will be used for equity, but that percentage will change depending on the group, as well as each shareholder physicians’ future goals. This is to maintain alignment with the overarching platform, and it allows shareholders to partake in the overall growth strategy of the private equity sponsor. A successful partnership will see shares appreciate until the 3 to 7-year growth cycle is completed, leading to the first liquidity event.

When considering a private equity partnership, the economics of the transaction become a moot point if the clinical and strategic fit is not right. In the current landscape of healthcare investment, doctors must continue to operate in an environment that leads to the highest quality outcomes for patients. Without this, a platform will struggle to find success in the long term. By developing a proper partnership plan, generating a sustainable and optimal growth strategy will come seamlessly with the right capital backer.

Physician Growth Partners is a firm that recognizes and prioritizes the importance of clinically focused outcomes, first and foremost. Groups that we have had the opportunity to advise will attest to the emphasis we place on prioritizing the partnership fit over the economics of a transaction.