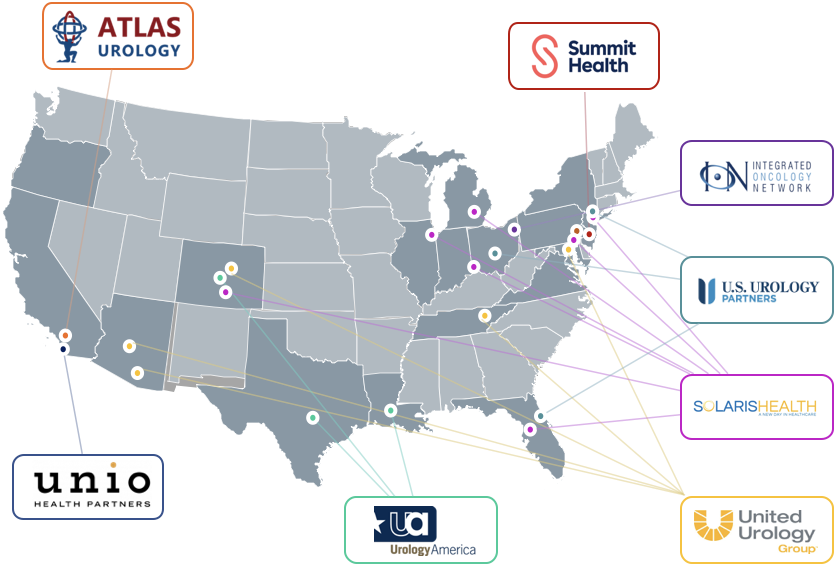

In the past three years consolidation within urology has shifted from nascent in nature to a pervasive force across the specialty, and it now serves as one of the most rapidly consolidating specialties in healthcare. Unlike earlier consolidation waves within dermatology, eye care, and dental, the dynamics of the urology space (large, independent group practices, deep shareholder bases, national connectivity through LUGPA) coupled with the rapid pace of activity has prevented many new private equity-backed platforms from forming. Instead of 30-40+ active platforms as we’ve seen in some other specialties, we only see eight true players in urology.

Additionally, in terms of market saturation and maturation, what took seven years to happen within dermatology and eye care has taken only three years within urology. The result of these market realities is a tightening window for independent groups to move on their own volition. Another unique component of urology consolidation is the creation of physician-led MSO models that serve as a private equity alternative. These physician-led groups have started to become a viable option for independent practices, but offer an entirely different set of pros and cons.

We expect urology consolidation to continue at a strong pace throughout 2023 despite changing economic conditions. While the opportunity to be a first mover has passed, independent groups now have the benefit of evaluating platforms with a proven track record. And while the opportunity for practices to partner with best-in-class MSOs isn’t going anywhere, ongoing, rapid consolidation will lead to continually changing dynamics that need to be considered.

Interested in how private equity can be helpful in your practice?